Table of Contents

Introduction: The Cash Flow Paradox That Stalls Growth

Construction firms are profitable. They’re not failing for lack of margin. They’re failing for lack of cash.

Here’s the statistic that reveals the paradox:

70% of construction firms rate cash flow as their primary concern. Yet only 12% use formal cash flow forecasting beyond a simple spreadsheet.

Firms are managing a critical constraint reactively instead of predictively.

The result? Missed growth opportunities. Higher financing costs. Strained supplier relationships. All preventable with visibility.

Your cash flow is volatile because the inputs and outputs of construction don’t align. You incur costs throughout a project. You bill at the end. Customers pay 30-60 days after billing. But your payroll happens every week. Your suppliers demand payment every 30 days.

Why Construction Cash Flow Is Inherently Volatile

Construction cash flow volatility isn’t a mistake. It’s structural.

- First: Timing Mismatch. You invoice based on milestone completion. But you pay suppliers for materials upfront. Equipment is financed before the project starts. Labor is paid weekly. But you might not invoice until the project is substantially complete. That’s 4-12 weeks of costs incurred before any invoice is generated.

- Second: Collection Timing. Even after invoicing, you wait. Industry-standard terms are Net 30. But most customers take 45-60 days. Government contracts take even longer—sometimes 90+ days.

- Third: Seasonal Patterns. Construction isn’t evenly distributed. Weather affects timing. You might have five projects starting in spring and only two in winter. That creates seasonal cash trough periods.

- Fourth: Unexpected Variance. A major customer delays payment by 30 days. A project gets postponed. Equipment breaks down and needs emergency rental. Scope changes require materials reordering.

The combination creates chaos. Some weeks you have ₹7.6 crore. Other weeks ₹1.42 crore. You can’t plan for that. You can’t invest. You can’t commit to growth.

The Cost of Cash Flow Blindness

Cash flow volatility isn’t just uncomfortable. It’s expensive.

- Financing Costs. Most firms maintain revolving credit lines to buffer cash swings. A ₹4.75 crore line at 8% annual interest costs ₹38 lakh per year. But if you’re actually drawing on it for 8-12 weeks of the year, you’re paying roughly ₹7.6 lakh-₹11.4 lakh in annual interest just managing volatility. That’s margin you didn’t have to lose.

- Growth Delays. You see an acquisition opportunity. A new market you could enter. New equipment you could buy. But you don’t have the cash. You wait. The opportunity passes. Competitors move in. You stay the same size year after year while others grow.

- Supplier Relationship Strain. Suppliers want reliability. You pay on day 30 for three months. Then month four, you pay on day 60 because of a cash trough. Suppliers respond by raising rates or demanding deposits. Your cost of goods goes up because of payment inconsistency.

- Missed Early Payment Discounts. Many suppliers offer 2% discounts for payment in 10 days. You can’t access those discounts when cash is tight. Over a year, that’s 1-2% margin lost just because you can’t manage cash predictability.

For a mid-sized firm with ₹190 crore in annual revenue, these costs add up: ₹9.5 lakh-₹14.25 lakh in financing, ₹1.9 crore-₹3.8 crore in missed growth investments annually, ₹47.5 lakh-₹95 lakh in supplier premiums. Total: ₹2.47 crore-₹4.89 crore in annual cost from cash flow blindness.

The cost of cash flow blindness (₹190 crore-revenue firm)

| Cost driver | Annual cost |

|---|---|

| Financing | ₹9.5 lakh – ₹14.25 lakh |

| Missed growth investments | ₹1.9 crore – ₹3.8 crore |

| Supplier premiums | ₹47.5 lakh – ₹95 lakh |

| Total | ₹2.47 crore – ₹4.89 crore |

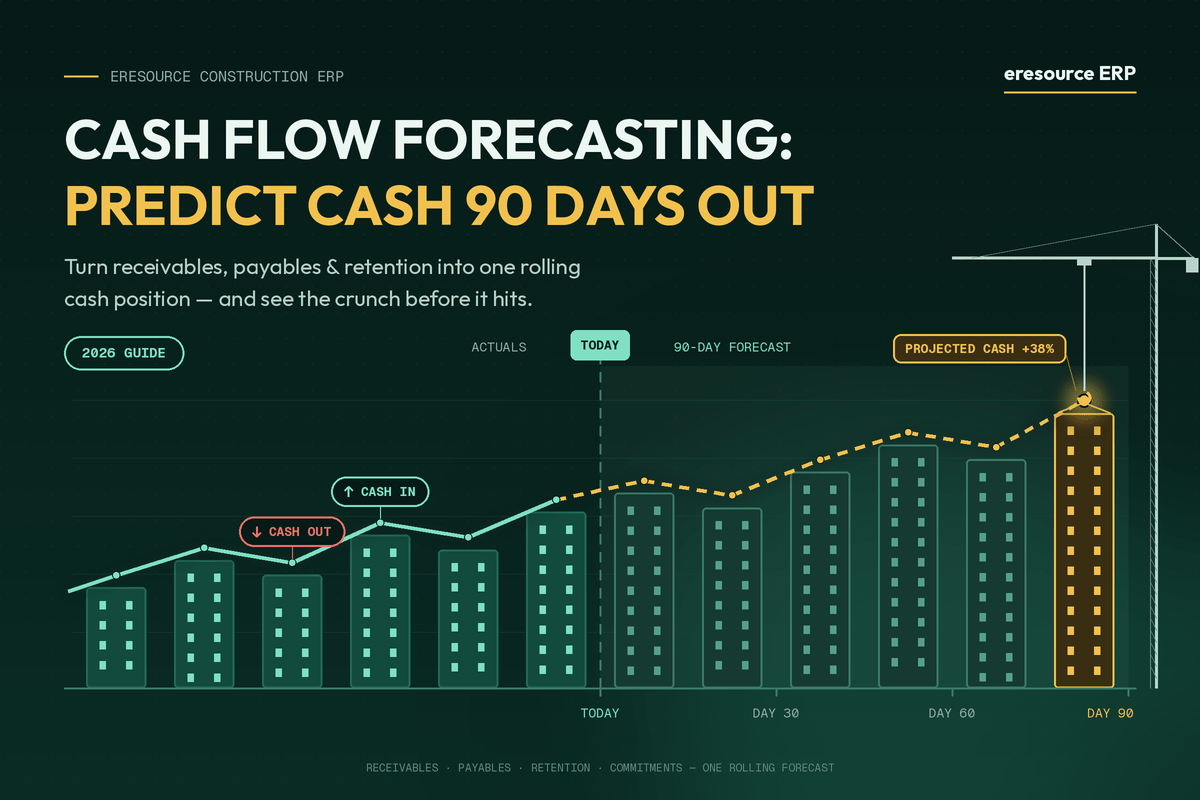

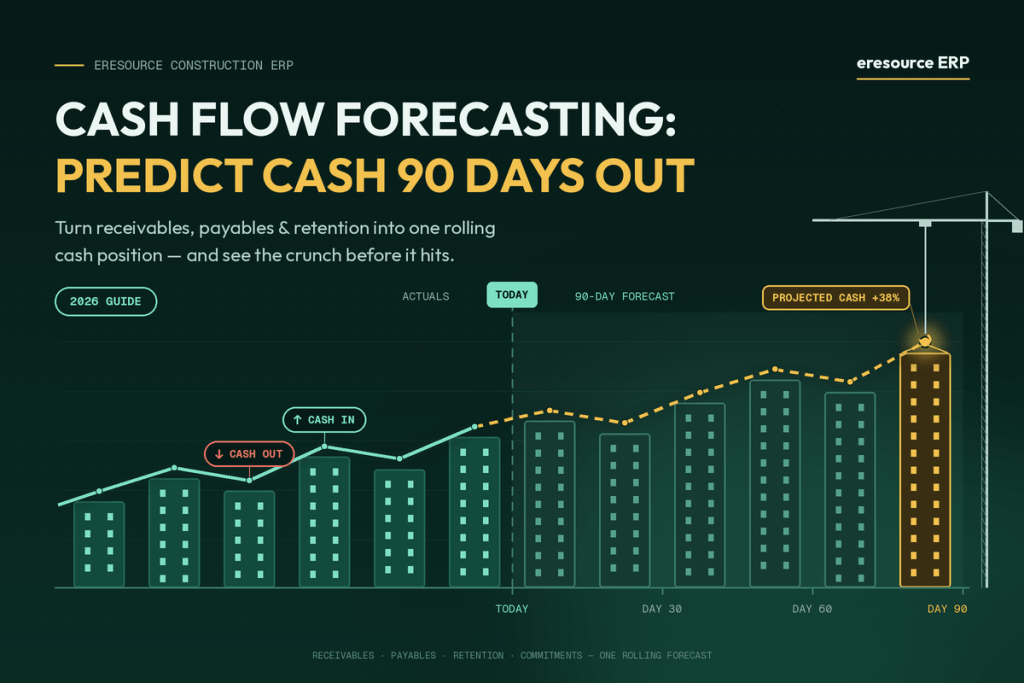

Inflow Modeling: Tie Revenue to Actual Payment Timing

Cash flow forecasting starts with inflows. You need to know when cash actually comes in, not when you invoice.

Inflow modeling means linking revenue invoices to customer payment history and contract terms. Not all customers pay on Net 30. Government contracts might be Net 45 or Net 60. Repeat customers have different patterns than one-time clients.

You build a model that says: Project X will invoice ₹4.75 crore. Based on this customer’s history, 70% arrives in 45 days, 25% in 60 days, 5% takes 75+ days. That gives you a cash inflow forecast for the next 90 days tied to reality, not assumptions.

The result: You know exactly when cash is arriving. You can plan outflows against actual inflow timing.

Also Read: ERP for Construction Industry

Outflow Planning: Schedule Costs by Date

Outflows are more predictable than inflows. Labor happens every Friday. Suppliers invoice monthly. Equipment rentals are quarterly.

Outflow planning means scheduling every major expense by the date it actually hits your account. Not the invoice date. The payment date.

You model: Labor costs ₹28.5 lakh per week. That’s ₹1.14 crore monthly, paid every Friday. Supplier invoices ₹38 lakh per month, due day 30. Equipment rental is ₹9.5 lakh quarterly, due on the 15th. Material costs spike in Week 3-5 of each project.

Outflow schedule at a glance

| Expense | Amount | Timing |

|---|---|---|

| Labor | ₹28.5 lakh/week (₹1.14 crore/month) | Every Friday |

| Supplier invoices | ₹38 lakh/month | Due day 30 |

| Equipment rental | ₹9.5 lakh/quarter | Due on the 15th |

| Material costs | Spike | Weeks 3-5 of each project |

With inflows and outflows modeled, you see the cash position week by week. Week 1: Outflows exceed inflows (cash dips). Week 4: Major customer payment arrives (cash rises).

Seasonal Adjustments: Account for Timing Patterns

Construction has seasonal patterns. Winter slows down. Spring is busy. This affects cash flow.

You might have five projects starting in March and two in November. That’s a seasonal inflow difference. Same applies to outflows. Winter requires less labor on outdoor projects but more indoor work on site prep.

Seasonal adjustments in your cash flow model account for these patterns. The model doesn’t assume even cash distribution throughout the year. It reflects reality: busy seasons with strong cash inflows, quiet seasons with thin inflows.

This prevents the surprise. You know January-February will be tight. You plan for it. You maintain higher cash reserves. You negotiate credit line availability before the trough arrives.

Scenario Modeling: What-If Analysis for Uncertainty

Your base forecast assumes normal timing. But construction is full of surprises.

Scenario modeling builds in contingencies. What happens if your largest customer delays payment by 30 days? Your forecast shows a cash shortage in Week 6. You plan for it now.

What if a new project starts two weeks early? Scenario modeling shows you have the cash to mobilize. You can commit confidently.

What if material costs spike 15%? You model the impact. You adjust cash reserves accordingly.

Scenario modeling isn’t prediction. It’s preparedness. You’re not guessing at what might happen. You’re planning for multiple possibilities.

Implementing Cash Flow Forecasting: Your Roadmap

Step 1: Audit Historical Cash Patterns. Review 12 months of bank statements. When does cash actually arrive? When do payments actually go out? Build a baseline of reality.

Step 2: Document Payment Terms by Customer. Not all customers are Net 30. Document actual payment timing for your top 10 customers.

Step 3: Schedule All Outflows by Date. List every recurring expense: payroll, supplier payments, equipment rental, insurance. Schedule by actual payment date, not invoice date.

Step 4: Model Project Invoicing. For each active project, when will invoicing happen? What’s the expected amount?

Step 5: Build Your Base Forecast. Combine inflows, outflows, and timing into a 90-day rolling forecast.

Step 6: Add Seasonal Adjustments. Overlay seasonal patterns to account for busy and slow seasons.

Step 7: Run Scenarios. Model best case, worst case, most likely case for major uncertainties.

The Payoff: Predictable Cash, Confident Growth, Lower Costs

Firms implementing cash flow forecasting eliminate cash volatility surprises. They move from reactive cash management (hoping payments arrive on time) to proactive planning (knowing when cash arrives and when it’s needed).

The payoff: Lower financing costs (credit line usage drops 30-50%). Confident growth investments. Better supplier relationships. Predictable cash for payroll. Negotiating power from reliable payment patterns.

Most importantly, you stop managing crisis-to-crisis. You start planning growth.

Learn Advanced Forecasting from Top Finance Teams

Free Cash Flow Mastery Webinar

Frequently Asked Questions(FAQs)

Because costs and payments don’t line up. You incur costs throughout a project but bill at the end, customers pay 30-60 days after billing (sometimes 90+ days on government contracts), while payroll is paid weekly and suppliers demand payment every 30 days. Seasonal swings and unexpected delays add even more volatility.

It’s modeling when cash actually arrives and leaves—tying invoices to real customer payment history and scheduling outflows by their actual payment date—to produce a 90-day rolling view of your cash position instead of reacting week to week.

For a firm with ₹190 crore in annual revenue, the costs add up to roughly ₹2.47 crore to ₹4.89 crore a year: ₹9.5-14.25 lakh in financing, ₹1.9-3.8 crore in missed growth investments, and ₹47.5-95 lakh in supplier premiums.

Inflow modeling links each invoice to that customer’s actual payment history and contract terms. For example, on a ₹4.75 crore invoice you might forecast 70% arriving in 45 days, 25% in 60 days, and 5% in 75+ days—giving a realistic 90-day cash inflow forecast instead of assuming everyone pays on Net 30.

Firms move from reactive cash management to proactive planning: credit line usage drops 30-50%, growth investments become confident, supplier relationships strengthen, and cash for payroll becomes predictable—so you plan growth instead of managing crisis to crisis.